What's the difference between scope 1, 2 and 3 emissions?

Scope 1, 2, 3 emissions are a way of categorizing emissions popularized by the GHG Protocol (the defacto standard for measuring carbon emissions that all businesses and standards use).

This categorization is used to delineate which emissions are a direct result of owned operations vs the emissions that are occurring in your service or supply chains – also known as your value chain.

Scope 1 emissions are directly created by your business (think of the vehicles you own, or a boiler in your office). Scope 2 emissions specifically relate to imported energy – like the electricity you buy to run your computers.

Last but not least: Scope 3 emissions are all of the indirect emissions that occur because of your value chain, but are not directly owned or controlled by you. This includes the goods you buy from your suppliers and vendors, and the emissions cause by your products when customers use them.

Here’s a great video that explains the difference between scope 1, 2 and 3 emissions.

As more companies strive to hit net-zero targets, meet changing regulations and keep up with increasingly sustainably-focused customers, measuring Scope 3 emissions is now a priority – and a challenge.

Scope 3 emissions often have the biggest impact on your overall climate impact. While the GHG Protocol defines 15 different categories of Scope 3 emissions, you can think of them in two general categories: upstream and downstream.

For an explanation and examples of all 15 categories, check out the resources at the end of the article here.

Upstream

These emissions are created in the production of your products or services. For example: the extraction of raw materials, the waste generated in the process, and the transportation of any of those materials or products.

Downstream

Downstream emissions happen after the product is made, and accounts for how that product will be used and discarded. These include shipping to customers and the disposal of your product at the end of its usable life.

Why is it important to measure your Scope 3 Emissions?

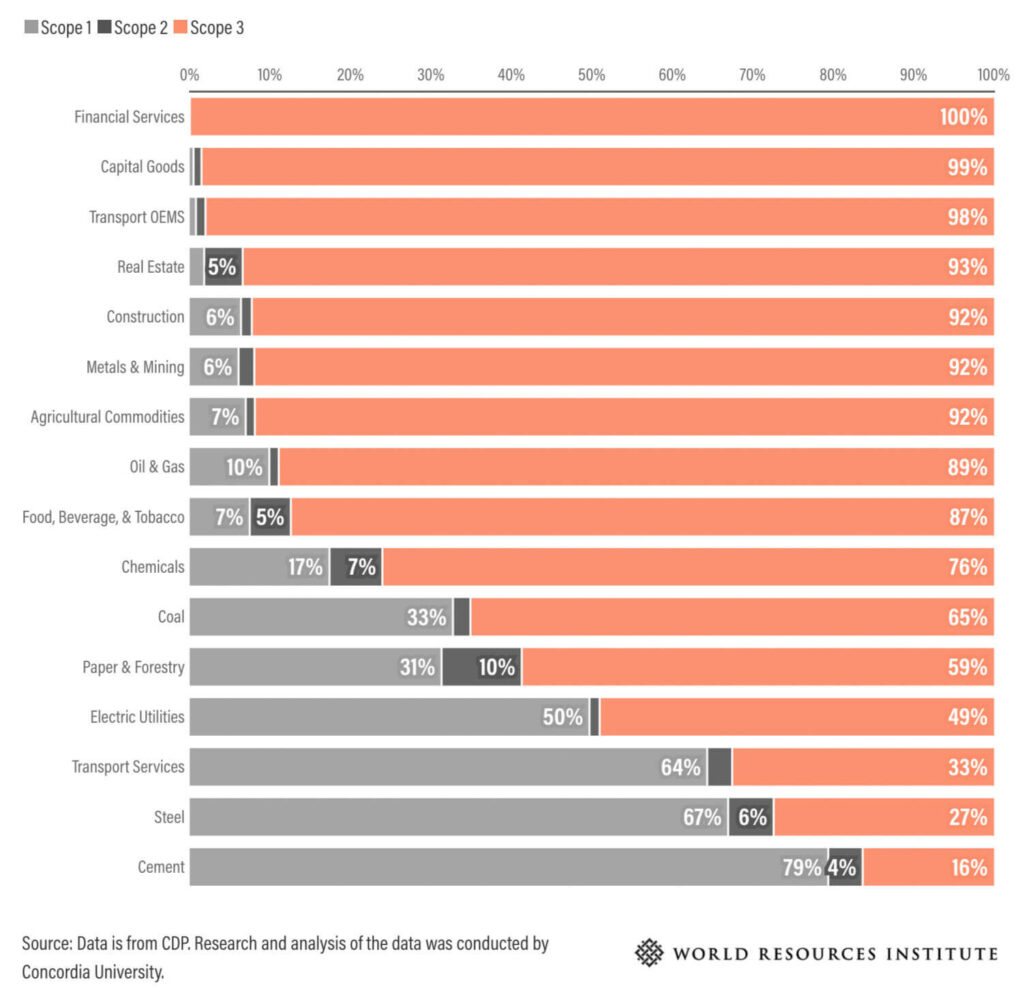

Scope 3 emissions make up around 90% of the average company’s total carbon footprint according to the CDP (see chart below), but can vary widely based on the industry, the hardest to measure with confidence, and the hardest to control.

So why bother at all? Here are a few reasons why:

Based on your location and industry, you might already be legally required to report your Scope 3 emissions. If you aren’t yet – you may have to soon!

Most regulations take a staggered or tiered approach to reporting requirements when it comes to Scope 1, 2, and 3 emissions. For example, OSFI (Office of the Superintendent of Financial Institutions) recently announced that they will require the major banks in Canada to report on their Scope 1 and 2 emissions in 2024 and their Scope 3 emissions in 2025.

Achieving net-zero emissions means that a business either emits no greenhouse gas emissions or offsets all of its emissions. To achieve net-zero emissions, your Scope 3 emissions must be accounted for.

Canada has pledged to meet its Paris Agreement goal to reduce greenhouse gas emissions by 40 to 45 per cent from 2005 levels by 2030. It has committed to achieve net zero emissions by 2050 – and businesses will be a major part of this commitment.

Reducing your impact builds a stronger brand, contributes to a more sustainable world, and can unlock new opportunities in markets that are prioritizing (and demanding!) sustainability-minded companies.

Employees, customers, investors and new talent are all increasingly looking for companies who have strong environmental values and practices.

Greenwashing is when companies give a false impression of how environmentally-friendly or sustainable they are. Without calculating Scope 3 emissions, companies might intentionally or accidentally be greatly underestimating their impact.

For example, while over 70% of emissions from the steel industry are Scope 1 and 2 (i.e. internal), 93% of emissions from the real estate industry fall in the Scope 3 category.

Automotive Properties REIT was able to quantify all of their Scope 1, 2, and 3 emissions under their operational control with Carbonhound without on-staff experts.

How do you measure (and reduce) your Scope 3 emissions?

Before you can reduce your Scope 3 emissions, you first have to measure them. This can be difficult, because they are outside of your direct control.

To calculate your carbon footprint, it is easiest and most efficient to use a carbon accounting platform. Carbon accounting is the process of quantifying your business operations in terms of its impact on the climate.

Some comprehensive and high-integrity solutions like Carbonhound can also automate much of the data collection that you need to account for your Scope 3 emissions.

Automate your carbon accounting and data collection

Calculate your footprint, manage your climate impact, set targets, and track your progress – all in one place.

To reduce your Scope 3 emissions, you will likely have to engage with your supply chain. That means working with your vendors and suppliers to understand where they are at in their climate journeys and ultimately reduce their emissions.

Some organizations will start with high level estimates, based on global averages or sometimes industry specific averages. This can be good as a starting point, but as soon as you look to reducing your emissions and start making decisions on procuring lower carbon alternatives, you will need to move to getting more supplier specific data or you won’t be rewarded for your climate action.

As a result, its always best practice to work with your suppliers to get their data initially so you have a better understanding of how they compare to industry averages and where you should be focusing your efforts.

Scope three can be daunting at first, but the hardest part is just taking the first step! Let us know if you need any help on your climate journey.

– The Carbonhound Pack

Resources

What are the Scope 3 emission categories?

The GHG protocol separates Scope 3 emission sources into 15 different categories, and how relevant and important each category is to your business completely depends on your operations.

The industry, operations, and context of your business all impact how these categories are used to calculate your climate impact.

Category 1: Purchased Goods and Services

These emissions are generated from the production, transport, and disposal of goods and services purchased by the organization. This includes raw materials, components, and finished products. Some examples are: paint, cleaning supplies, paper, pens, and feedstock.

Category 2: Capital Goods

Emissions in this category are a result of the production, transport, and disposal of capital goods. Think of the buildings, machinery, and infrastructure, that are purchased or leased by the organization.

Category 3: Fuel and Energy Related Activities

These emissions arise from activities not included in Scope 1 or Scope 2 emissions, such as the extraction, production, and transportation of fuels and energy used by the organization. It captures the upstream emissions from your purchased fuels, electricity, transmission and distribution losses, and sold electricity.

Category 4: Upstream Transportation and Distribution

These emissions are associated with the transportation and distribution of products and materials from your suppliers to the organization. Basically, this includes shipping, logistics, and freight – so long as the vehicles aren’t owned by your company.

Category 5: Waste Generated in Operations

Category 5 emissions result from the waste generated during your organization’s operations including solid waste, wastewater, and hazardous waste. Examples include landfill disposal, recycling, incineration, composting, waste-to-energy (WTE) or energy-from-waste (EfW), and wastewater treatment.

Category 6: Business Travel

This one is pretty simple: it’s just the emissions that are produced by your employees’ business travel. It includes air travel, road transport, taxi, and rail travel.

Category 7: Employee Commuting

These emissions arise from employees’ commuting to and from work. Whether it is by car, public transportation, or other means, companies can also include emissions from employees who work from home or remotely.

Category 8: Upstream Leased Assets

Emissions in this category are associated with the production, transport, and disposal of assets that the organization leases, such as vehicles or equipment.

Category 9: Downstream Transportation and Distribution

These emissions occur due to the transportation, storage, and distribution of products from your organization to your customers, specifically if that process occurs in vehicles/facilities not owned by you. Examples would be a leased warehouse, distribution centre, or rail and air transport of your goods to your customers.

Category 10: Processing of Sold Products

Category 10 emissions are generated from the processing of products sold by third parties (i.e. contract manufacturers) after you sell it. An easy way to think about it is the emissions created when sugar you sell is turned into candy.

Category 11: Use of Sold Products

These emissions are a result of how your customers use your products. It includes the energy consumed by operating or maintaining your product. Companies are required to report direct use-phase emissions, but indirect use-phase emissions are optional. This category applies to products that directly consume energy such as engines, motors, lights, etc. as well as products that indirectly consume energy such as clothing, food, and pots and pans.

Category 12: End-of-Life Treatment of Sold Products

Emissions in this category are from the disposal or treatment of your products once they reach the end of their useful life. This includes recycling, landfilling, or incineration.

Category 13: Leased Assets

If your company leases any assets to third parties, these emissions account for the impact of those assets. For example, a company that leases vehicles may need to request fuel or mileage data from the people who lease their cars in order to calculate emissions.

Category 14: Franchises

Category 14 includes emissions from the operation of franchises not included in Scope 1 or Scope 2. A franchise is a business operating under a licence to sell or distribute another company’s goods or services within a certain location. This category is applicable to franchisors

Category 15: Investments

This category includes Scope 3 emissions associated with your company’s investments that are not already included in Scope 1 or Scope 2. It is most applicable to investors and companies that provide financial services. It also applies to investors that are not profit driven (e.g. development banks).