Public companies face increasing pressure from investors, customers, and stakeholders to be accountable for their climate impact and to report on their climate-related risks. In the US, the SEC has recently updated their Climate-Related Disclosure Rules to reflect the need for consistent, comparable, and reliable information about the financial effects of climate-related risks – including a company’s greenhouse gas emissions.

The Enhancement and Standardization of Climate-Related Disclosures Rules from the SEC cover topics like board oversight of climate risks, the impact of climate on the business to date, and a business’ carbon footprint.

So what are the new rules when it comes to emission reporting? In short, greenhouse gas accounting is not required for any company unless it is deemed a material risk that needs to be disclosed. This might have some businesses breathing a sigh of relief, but the reality is that they are not totally off the hook.

Ok, then why do greenhouse gas emissions still matter? Per the SEC’s final rules, “the most common reason asserted for supporting the mandatory disclosure of GHG emissions is that such disclosure would provide investors with specific metrics to assess a registrant’s exposure to transition risks.” What that fundamentally means is that credible greenhouse gas emissions accounting provide a solid, measurable foundation to assess a business’ ability to be successful and sustainable as they transition to a low-carbon future.

Who do the new rules apply to?

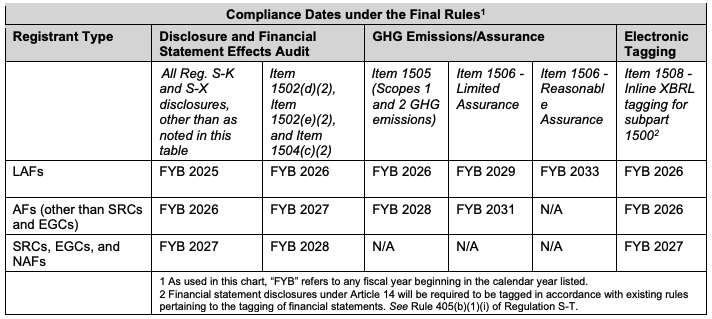

The rules apply to public companies registered with the Securities Exchange Commission. Based on the type of registrant, the timelines and rules vary. Below are the different types of registrants:

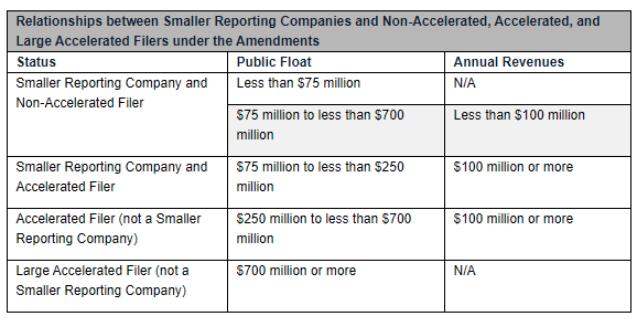

- Accelerated Filer (AF): a reporting company that has a public float of between $75 million and $700 million

- Large Accelerated Filer (LAF): a reporting company that has a public float of $700 million or more

- Non-accelerated Filer (NAF): a reporting company that does not meet the requirements of a large accelerated or an accelerated file

- Smaller Reporting Company (SRC): a reporting company that is not an investment company, an asset-backed issuer, or a majority-owned subsidiary of a parent that is not an SRC.

- Emerging Growth Company (EGC): an election that a newly public company can make, which offers the company certain benefits

What do the new rules cover?

You can find the full list of the disclosure requirements on the fact sheet, but here is a summary of the governance and risk topics covered:

- Material climate-related risks

- Activities to mitigate or adapt to those risks

- Information about the registrant’s board of directors’ oversight of climate-related risks and management’s role in managing material climate related risks

- Information on any climate-related targets or goals that are material to the

registrant’s business, results of operations, or financial condition (e.g. carbon emissions, natural disaster, or other relevant metrics)

When do public companies need to disclose their greenhouse gas emissions?

Importantly, the SEC Rules require that public companies disclose their greenhouse gas emissions starting for the Fiscal Year 2026 for Large Accelerator Filers (LAFs). All regulated companies will have to start with their material Scope 1 and 2 emissions, and eventually work towards limited and reasonable assurance on that data.

Source: The Enhancement and Standardization of Climate-Related Disclosures: Final Rules Fact Sheet

What is limited vs reasonable assurance?

When a company has its greenhouse gas emissions data reviewed by a third-party, there are different levels of assurance that the third-party can give. They represent the overall quality, integrity, and credibility of the data.

Limited and reasonable assurance describe how certain the auditor is that the information in the report is materially correct, and that the information that is included is relevant to the company’s business.

A reasonable level of assurance that looks at the materiality reduces greenwashing and ensures that the company does not just focus on areas where it performs well.

Limited Assurance

A limited level of assurance on a report relies mostly on the data that the company provides themselves, rather than digging too far into the original sources of data. There is some verification of those sources (documents, invoices, etc.), but there is less scrutiny and the materiality of each topic that is included in the report is not assessed.

The auditor is not aware of any material modifications that should be made.

Reasonable Assurance

Reasonable assurance looks more deeply into a company’s internal processes and controls. The auditor checks the metrics and disclosures, and traces the data back to its original source to confirm its accuracy.

The auditor will also look at the materiality of the data included to make sure that the company’s report focuses on the relevant items.

The auditor affirms that the information in the report is materially correct.

Where does carbon accounting software fit in?

Measuring and reporting on greenhouse gas emissions (carbon accounting) is a critical first step towards understanding a business’ impact, striving towards climate action and complying with the SEC Rules.

Greenhouse gas emissions are one of many metrics that could be considered in a company’s climate risk report, and without quality emissions data, governance bodies can’t effectively manage their climate risk.

The complex modelling that is required to translate an organization’s operations into qualitative physical and transition climate risks requires credible data to back it up. This is where technology and software comes in.

Plus, since many companies don’t have an in-house sustainability expert nor massive budgets to spend on consultants every year, carbon accounting software like Carbonhound is a no-brainer. With transparent and accessible pricing and an automated interface designed for anyone, it is the best way for companies to take control of their climate data with confidence.

Tendril Studio and Forever Co. prepared a response to their customer’s emissions reporting request in just three weeks.

What comes next after the SEC climate disclosure rules?

With the new rules in place for Scope 1 and 2 emissions, Scope 3 emissions disclosure requirements are on the horizon. Plus, other international regulations like the EU’s Corporate Sustainability Reporting Directive (CSRD) require non-European companies that generate over €150 million in the EU to report on their Scope 1, 2 and 3 emissions.

Companies that do business in California may also be impacted by the California bills SB-253 and SB-251, which require disclosure of their full value chain (Scope 3) emissions.

Leveraging carbon accounting software gives companies visibility into every corner of their business from a carbon emissions lens – including their Scope 3 emissions – to be prepared and confident in their compliance with US and International climate reporting regulations.

Resources

What is the SEC?

The Securities and Exchange Commission (SEC) is a U.S. government oversight agency that regulates the securities markets and protects investors. Is was established in the U.S. Securities Act of 1933 and the Securities and Exchange Act of 1934, largely in response to the stock market crash of 1929.

Their mission is to to protect investors; maintain fair, orderly, and efficient markets; and facilitate capital formation.

What is the relationship between different SEC filing statuses?

Automate your carbon accounting and data collection

Calculate your footprint, manage your climate impact, set targets, and track your progress – all in one place.